Profit is not the problem with American healthcare

Health insurance companies are closer to scapegoats than murderers.

Discussion continues about the United Healthcare CEO shooting and problems with U.S. healthcare generally. Much of that discussion seems driven by a view that I find simplistic, inaccurate, and colored by subconscious bias. Rather than relitigate whether killing is bad, I’d like to try to complicate that view, explain why it’s unhelpful to healthcare reform, and extend that insight to broader patterns of political sense-making.

The view I’m referring to goes something like this:

The main reason U.S. healthcare is so much more expensive, complicated, and non-universal than healthcare in other rich countries is that it puts “profits before people.” It is a for-profit capitalist system, whereas other countries have shifted to more humane socialized systems.

The specific entities placing profits before people are mainly private insurance companies, which is why we need Medicare for All. The whole business model of private insurance is to collect more money from premiums than they give out in payments, which seems innately extractive. Plus, it creates incentives to deny as many claims as they can get away with and erect byzantine coverage networks that make the whole process of seeking and paying for care a confusing hassle. By contrast, Medicare for All allegedly saves on administrative costs and complexity and gets rid of the profit incentive to deny coverage.

Abusive profit-seeking is especially outrageous in healthcare/insurance compared to other sectors because so many lives and QALYs are on the line. Decent societies should care for sick people regardless of their ability to pay. To deny or limit coverage for potentially life-saving care so that your CEO can pay himself a $10 million salary feels morally similar to murder—and also theft, since that person already paid into your coverage for just such a contingency.

Therefore, health insurance CEOs are a special kind of evil, and I sympathize with anyone standing up to them. While most with this view stop short of condoning vigilante assassinations, they also feel that this Brian Thompson guy probably had it coming for rejecting so many claims.

Luigi Mangione hinted at this view in his notebook minifesto confessing to the killing, and I understand why it appeals to many people. It’s digestible and superficially reasonable.1 It’s simple enough to understand and remember, but complicated enough to make people think they’ve done their homework. Best of all, it validates the left’s foundational suspicion that the world’s main problem is greed. It pairs a causal explanation for an observable phenomenon with a strident moral judgment against the exact type of person or activity they are predisposed to condemn.

I have my own biases, of course. And I’m not a health policy expert, so the views below may oversimplify in their own way. Still, I think I know enough to make a persuasive case that the narrative above is wrong. At minimum, I should be able to convince you that Luigi Mangione wasn’t just wrong to kill Brian Thompson, but also wrong to blame Brian Thompson for why, in his words, “the US has the #1 most expensive healthcare system in the world, yet we rank roughly #42 in life expectancy.”

My argument has two parts. Part I, here, will give some initial reasons to be skeptical of the “profits over people” narrative. Part II will provide a more plausible explanation for why U.S. healthcare is so messed up, and close with an appeal to Luigi Mangione sympathizers.

1. Health insurance profits are far too small to explain why U.S. healthcare is so expensive.

The United States spent $4.9 trillion on healthcare in 2023, or $14,570 per person. The average country with our GDP spends about half that. Any theory for why Americans pay so much needs to account for about 50% of U.S. healthcare spending.

Health insurance company profits represent about 0.5% of U.S. healthcare spending. 0.005 of the total. They also run lower profit margins than most other industries: around 3%, whereas the average profit margin of companies on the S&P 500 is about 12%.

Some large insurers in the U.S. are even nonprofits, including Kaiser Permanente and many members of Blue Cross Blue Shield.2 The insurance industry hardly seems to be profiteering, and its profit cannot begin to explain the inflated cost of U.S. healthcare unless it’s through downstream effects unrelated to the profits themselves.3

2. Many health systems that do offer universal coverage also have for-profit insurance and care.

Australia, France, Germany, the Netherlands, Sweden, and Switzerland all have universal coverage, and all offer varying but meaningful amounts of that coverage through private, for-profit insurance companies. For-profit hospitals are also found in all six nations, again to varying degrees.

Moreover, the U.S. health system is much less private than most people think. Only about 30% of U.S. healthcare spending passes through private insurance. State and federal governments directly pay for roughly half of U.S. healthcare costs through Medicare, Medicaid, and Veterans Affairs, a figure which is growing over time. That figure rises to about two-thirds when you include public employees’ health benefits and tax subsidies to private health spending. I’ll say that again: two-thirds of U.S. healthcare is ultimately paid for by the government, in this allegedly laissez-faire system of ours.

The truth is that most healthcare systems are a mixture of public and private providers and payers, and the United States is not really an outlier in terms of how much of its spending is public or private.4 Yes, U.S. healthcare is less “government-run” than most competing models in the sense that a) health insurance is not compulsory, since the elimination of the individual mandate,5 and b) there are fewer price controls, which I’ll return to later. But healthcare is still one of the most heavily regulated sectors of the economy and very far from a free market.

3. Greed alone cannot explain why healthcare is so uniquely expensive in a broadly profit-driven economy.

All corporations seek to maximize profit. Insurance and pharmaceutical executives may be greedy, but there’s no reason to think they are greedier than those at Nike or Amazon. And again, even if they were, they have not converted that greed into abnormal profits. Biopharma’s profit margin is about 17%, which is above average but not an outlier: “significantly lower than Computer Sciences (31.6%), Beverages (27.4%), Aerospace/Defense (23.0%), and Trucking (19.1%)”.

Most products sold for profit are relatively affordable and could not be profitable otherwise. Yes, demand for some healthcare is inelastic—if you’re sick enough, you “can’t say no”. But most patients’ circumstances are not so dire, and demand for preventative healthcare is sensitive to out-of-pocket cost. Besides, people “can’t say no” to shoes, clothing, or basic food items either, but they can afford those products in abundance. In a healthy market, competition between providers is enough to restore consumers’ leverage and keep prices in check, even when consumers have to buy from someone.

Nor is insurance innately extractive in any other context. There is no cost spiral for life insurance, home insurance, renter’s insurance, or car insurance, even though all of those industries must also collect more in premiums than they pay out. That’s because those forms of insurance are understood to sell peace of mind against large but unlikely risks, whereas today’s health insurance has become mere prepayment for inevitable future consumption. More on that in part II.

4. Most of Americans’ excess health spending goes not to insurers, but to healthcare providers, including many who operate as nonprofits.

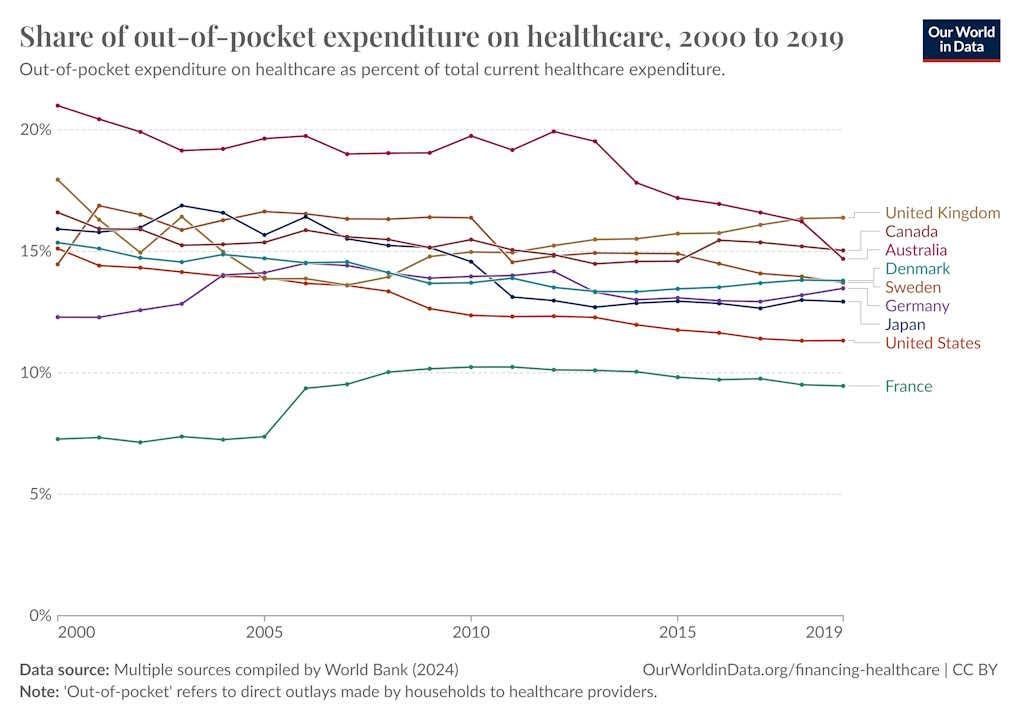

Noah Smith wrote a good explanation of why it’s wrong to blame insurance companies for America’s healthcare failings. Not only do insurance companies not make very much profit, but Americans pay a smaller percentage of their health bills out of pocket than do people in most rich countries. That is, private insurers pay more of our healthcare bills than do single-payer government insurers in countries like Sweden, Canada, or the UK.

If our insurers pay a larger percentage, but we still wind up paying more overall, who’s raking in the extra cash? Studies show that it goes to healthcare providers: “hospitals, pharma companies, doctors, nurses, tech suppliers,” etc. Smith summarizes:

“The fundamental reason your health care costs so much is not that the health insurance companies are lining their pockets. And it’s not that insurers are an inefficient mess. It’s that the actual provision of America’s health care itself just costs way too much in the first place…

Excessive prices charged by health care providers are overwhelmingly the reason why Americans’ health care costs so cripplingly much. But they’ve outsourced the actual collection of those fees to insurance companies, so that your experience in the medical system feels smooth and friendly and comfortable. The insurance companies are simply hired to play the bad guy — and they’re paid a relatively modest fee for that service.”

What allows U.S. health providers to charge such excessive prices? Tune into Pt. II to find out.

This is the part of the post where people will accuse me of straw-manning. If your own views on healthcare are significantly more sophisticated than those presented here, you don’t have to wear the shoe. This is not an attempted steelman. But I do think what I wrote is a fair representation of how most millennials or younger Democrats view the issue.

Take the 2019 Democratic primary debate by way of example (I’d cite the 2023 Democratic primary debate, but alas…). Senator Cory Booker lamented that "[t]here are too many people profiteering off of the pain of people in America, from pharmaceutical companies to insurers.” Senator Elizabeth Warren lamented how insurance companies "sucked $23 billion in profits out of the health care system” last year. And Senator Bernie Sanders pitched his plan’s strategy to lower costs as: "We will substantially lower the cost of healthcare because we stop the greed of the insurance companies.” Their basic messaging strategy is to convert sympathy for the sick into anger at the affluent because this is how their voters think.

Interestingly, Brian Thompson’s $10 million salary was actually lower than the $15 million salary of Kaiser Permanente CEO Greg Adams, despite the latter running a nonprofit. The debate over CEO pay is complicated and I won’t get into it here, but clearly it’s not only the profit motive that drives large organizations to give out these salaries.

If you’re shouting about administrative inefficiency, I’ll get there in part II.

Unless you count “publicly mandated,” but privately run and often for-profit, health insurance as “public.”

Obamacare’s failure to even dent our country’s steady increase in health expenditure underscores my point about how little this matters to what’s actually driving up costs.

One thing to keep in mind in the United States is that the tax code is structured such that most working people are effectively forced to get their health insurance through their employer. This creates all kinds of problems such as distortions in the labor market and a greater likelihood of insurance companies to deny claims to save money. After all, even if a health insurance company gets a bad reputation for wrongly denying claims, it’s not as if people with their policies can easily drop them for another company the way they could with say auto insurance. Other countries that do have private health insurance such as the Netherlands and Switzerland don’t link it to employment. That is a unique and very negative feature of the American system.

I will follow along here. Looking forward to part 2, which incorporates the providers of the care. For a later discussion, I’ve had discussions with a forensic accountant who works for our government to investigate Medicare fraud. According to her, the fraud is actually coming from Russia hacking into those funds and stealing them to the tune of BILLIONS. Only a very small fraction of that fraud is coming from within the US. I can’t corroborate this information with publications…